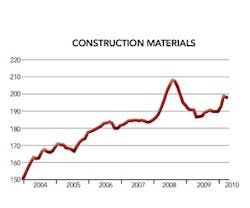

Prices for Construction Materials Stabilize

Overall, construction material costs are stabilizing and have seen an average increase of 2% to 3% over the past 12 months. Bucking the overall trend, lumber prices are down 1% to 2% over the last year, and may finally be bottoming out.

After a few ups and downs over the last 12 months, rubber and rubber products are registering increases in the 3% to 4% range, and stockpiles are dwindling. At publication time, the price of crude is high, which may add to the volatility in rubber prices. After big gains since 2004, sand and gravel have moderated to 1% to 2%. The highway portion of public works construction is causing the demand. Due to the weak housing, commercial, and public construction markets, millwork will likely remain flat. Prices for clay and ceramic products remain flat. Affected mostly by commercial and public building construction, limestone prices have been flat since 2006.